Is Battery Data the Key to Europe's Energy Storage Future?

Europe's battery debate often starts with supply. That makes sense. Raw materials, refining capacity, and geopolitical exposure are real pressure points.

But supply is only part of the story. Fragmented data is a second, quieter weakness in Europe's battery system.

Once battery assets move beyond first use, their value depends on tracking and tracing them.

It also depends on routing them to the best use-case. You must verify recovery and recycling to retain material value.

This depends on keeping relevant battery data connected across the lifecycle. This includes both static data and usage data.

That is a central argument in our new white paper, Build European Resilience: Data Defeats China's Geo-Controls.

The white paper describes Europe's exposure as both industrial and informational. It argues that resilience will depend not only on external sourcing. It will also depend on better circular data infrastructure.

Why the Battery Industry Can't Afford to Ignore Its Data Problem

The battery industry is at an inflection point. Across the entire battery value chain, data continuity is becoming as important as the physical supply.

This includes raw material extraction. It also includes manufacturing and deployment. It covers second-life use as well. It also applies to end-of-use recovery.

Yet most systems handling lithium-ion batteries today still treat data as a byproduct, not a core asset.

That gap is not a minor operational inconvenience. It is a structural weakness. When a lithium-ion battery is passed on, important data is often lost.

This can happen when it moves from the maker to the operator. It can also happen when it moves from the operator to the refurbisher. It can also happen when it moves from the refurbisher to the recycler.

This data covers its chemistry, condition, and history. It may also be locked in separate systems. The result is slower decisions, weaker recovery outcomes, and missed opportunities to retain material value inside Europe's own economy.

China's Position Makes the Challenge Hard to Ignore

That exposure becomes especially clear when looking at China battery market dominance across global supply. The International Energy Agency (IEA) says China now makes over three-quarters of batteries sold worldwide. China also holds a dominant position in key parts of the supply chain.

China’s battery supply chain goes beyond manufacturing. It covers key mineral refining and cell chemistry development. It also includes software and data systems that manage battery performance.

In 2024, battery prices in China fell faster than anywhere else. This widened the competitiveness gap with European battery storage producers and North American manufacturers.

China battery market dominance is not simply a manufacturing story. It is a systems story, and Europe's response needs to be one too.

Why This Matters Now

The pressure on battery supply chain Europe is no longer theoretical. It shows how the market talks about supply security, battery routing, recycling capacity, and domestic recovery.

Under the EU Battery Regulation, the battery passport applies from 18 February 2027.

The EU Batteries Regulation 2027 will change a lot.

For the first time, battery manufacturers and importers, as economic operators under the regulation, must provide detailed battery data. From chemistry, to composition, carbon footprint, and usage data during battery life. Accessible to anyone.

The European Commission Digital Battery Passport is the regulatory mechanism designed to make this happen. The EU battery passport framework requires economic operators across the battery value chain to keep and share structured data.

This includes manufacturers, importers, distributors, and downstream handlers. They must do this throughout the battery’s life. The battery passport EU requirement is not optional for compliance withepaperwork. It is a foundational shift in how the battery industry is expected to operate.

The travel direction is clear. Batteries in Europe are moving towards traceability, accountability, and structured lifecycle data. That regulatory shift matters.

But regulation alone will not solve the problem.

As our white paper argues, Europe’s resilience depends on data moving with the battery. It must move across handovers, decision points, and recovery pathways. That means better traceability, better integration, and better evidence for reuse, recycling, procurement, and compliance.

This matters because disconnected battery recycling data has practical consequences. It slows down decision making on battery second life vs. recycling. It weakens confidence in downstream battery flow quality.

It makes recovery outcomes harder to verify. And it limits Europe’s ability to make circularity a real industrial advantage, not just a nice policy phrase.

What Is the EU Battery Regulation Actually Asking For?

For anyone seeking clear guidance on the EU battery rules, here is the short answer. You need structured, accessible, and ongoing data across the full battery lifecycle.

The EU battery regulation sets out duties for all economic operators who sell batteries in Europe.

This includes manufacturers in Asia, importers across member states, and operators managing battery energy storage assets in Europe.

Under the EU batteries regulation 2027 timeline, compliance is not a future consideration. Preparation needs to start now.

The European Commission is developing a digital battery passport infrastructure.

It will act as a common data layer. It will provide a standard way to record and share battery information.

This will keep the data usable across the battery value chain. It will work regardless of which stakeholder holds the asset at any time.

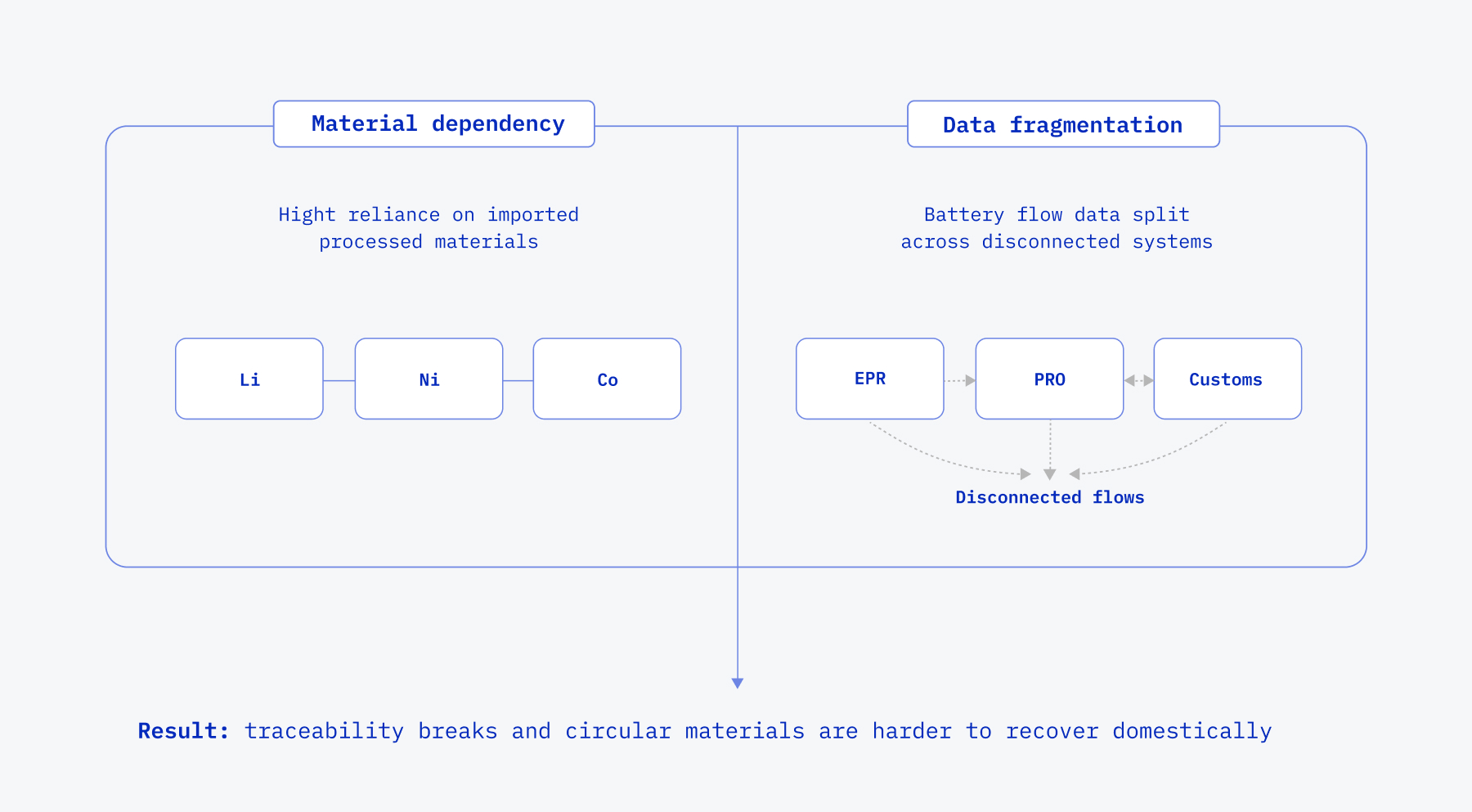

Europe's Real Challenge Is Twofold

Our white paper describes Europe's challenge as a combination of two linked vulnerabilities.

- The first is material dependency: ongoing reliance on foreign sources for key processed battery materials. China’s battery supply chain is the most concentrated single risk point.

- The second is battery data infrastructure: a system in which battery information is split across stakeholders, handovers, and regulatory touchpoints, making continuous traceability difficult. Without a shared battery data system, even strong recycling goals can fail.

The data to route, verify, and recover batteries is often missing. It is not available on time, for the right stakeholder, or in a usable format.

That combination matters. If Europe wants to retain more critical value domestically, it needs more than recycling ambition. It needs systems that make battery assets identifiable, traceable, and actionable from intake to routing to closure.

This broader pressure is also being voiced openly by industry observers. In a recent Batteries International opinion interview, Shmuel De Leon described the current moment as a structural shock.

He said it affects battery manufacturing outside China. He argued that overcapacity, price pressure, and reliance on Chinese supply chains are causing a deeper crisis.

He said Europe and North America face the worst of it. That is not the main basis of this article, but it does reflect a wider market mood: the concern is no longer abstract.

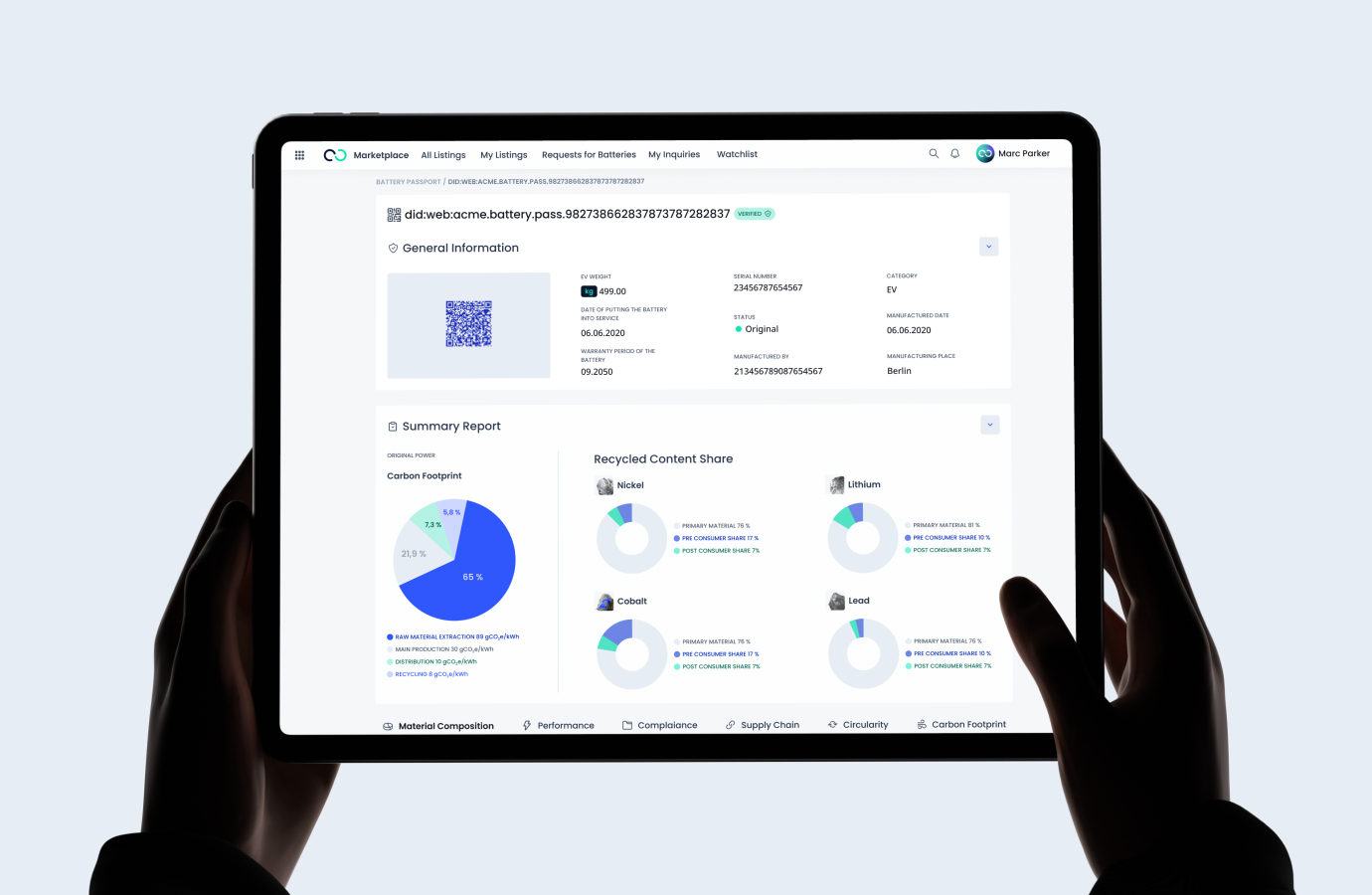

How Does the EU Battery Passport Work in Practice?

One of the most common questions in the battery industry right now is this. How does the EU battery passport work across the supply chain?

The EU battery passport is not a single document or a static certificate. It is a digital record, linked to a specific battery unit . It stays with the asset and updates dynamic information throughout its lifecycle.

Under the European Commission digital battery passport framework, this record must include:

- The battery’s chemistry

- The battery’s carbon footprint

- The battery’s state of health

- Data on what happens at the end of its first life

For economic operators managing lithium-ion batteries at scale, this creates both a compliance obligation and a practical opportunity. The obligation is clear: EU battery regulation requires this data to exist and be accessible.

The opportunity is less obvious but just as important. Batteries with complete, verified data are easier to route. They are easier to sell in second-life markets. They are also easier to recover efficiently.

This directly supports the economics of battery recycling data. It also supports circular material flows.

What Happens to Recycled Materials Without Good Data?

This is where battery recycling data becomes commercially significant, not just regulatorily relevant.

When lithium-ion batteries reach the end of their first life, people must decide what to do next.

They may reuse them, refurbish them, use them for a second life, or recycle them. These choices depend on what data is available.

If the data is missing or incomplete, choose the cautious option. Also choose the cautious option if the data is locked in a system that the next stakeholder cannot access. It is to recycle, even if value remains.

That is an economic loss. Recycled materials recovered from batteries that could have had a second life carry real costs. These costs are financial. They also reflect the energy and carbon used in the original manufacturing process.

Better battery recycling data means better routing decisions, which means more recycled materials are recovered at higher value, and fewer assets are downgraded unnecessarily.

The battery data infrastructure needed to support this does not have to be complex. But it must be connected across the battery value chain. It must also link economic operators and regulatory touchpoints set by the EU Battery Regulation.

What Battery Resilience Looks Like in Real Life

Battery resilience is not built in one grand move. It is built in handovers.

A battery leaves its first use. Then the real questions begin:

- What kind of battery is it exactly?

- What condition is it in?

- Can it be reused? Does it need repairs?

- Is it better suited for a second life?

- Or is it ready to recycle?

If the right information travels with the battery, those decisions become much easier. If it does not, the battery quickly turns into a black box.

That is where resilience becomes very practical. A battery should not arrive at the next stage of its life as a mystery package. It should come with an identity, condition of data, and the basic documentation needed to decide what happens next.

The same applies at the other end of the chain. If a battery is recycled, the outcome should not disappear into the fog. Recovery results, material yields, and proof of what happened must be clear and usable. The next stakeholder in the chain must be able to see them.

In simple terms, resilience depends on whether the battery keeps its "story" as it moves through the system. When the story is clear, we can assess assets faster. We can route them better. We can match them more easily to reuse, a second life, or recycling paths.

When the story gets lost, everything slows down. Decisions become harder; trust drops, and valuable materials are more likely to leak out of the system. That is why traceability matters. Not because it sounds nice in regulation, but because it helps the market work with less guesswork and more confidence.

From Hong Kong: What the Market Conversation Made Clear

Our team recently spent a few days in Hong Kong. We spoke with stakeholders across the battery and energy storage space. What those conversations made clear is that the underlying pressure is remarkably similar across markets.

Supply security, local value creation, project bankability, and credible pathways for reuse, recycling, and recovery are no longer regional concerns. They are shaping battery strategy far more broadly.

At the center of many of these discussions was a simple point: better decisions depend on better battery data. Without connected data across the lifecycle, it is harder to route assets well. It is also harder to verify recovery and keep material value visible.

That is why the argument of this white paper reaches beyond one region. Battery resilience depends more on supply volumes and on the quality of market systems behind them.

New White Paper: Build European Resilience

Our new white paper explores how Europe can respond more effectively to supply concentration and geopolitical pressure by improving the systems that connect battery assets, stakeholders, and recovery outcomes.

Inside, we cover:

- Europe's industrial and informational exposure

- Why fragmented battery data weakens resilience

- How circular data can support routing and recovery

- Five practical pillars for 2025 to 2027

- Audience specific playbooks for implementation

Go Deeper: Our Podcast on China and Battery Resilience

For readers who want the broader strategic context, we also recommend our podcast conversation on China and Europe's battery position. Circunomics has published the episode "China Tightens the Tap: How Europe Can Build Battery Independence."

It adds more context around tightening controls, Europe's position in the battery ecosystem, and the strategic importance of traceability and circular systems.

The conversation explores how export controls, recycling strategy, and stronger traceability systems are reshaping the resilience debate.

The Real Opportunity

Europe is unlikely to out-scale global battery powerhouses overnight. That is not how this machine works. But it can become better at something highly practical: turning battery data into action. That means stronger routing decisions.

Better recovery evidence. More confidence in second life and recycling pathways. Better procurement signals. And a better chance of keeping material value visible and usable inside Europe's own system.

That is the case where we make this white paper. Resilience is not only about securing more supply. It is also about building better visibility, better continuity, and better battery outcomes across the lifecycle. And that is also why this conversation matters commercially.

A battery market works better when assets are easier to identify, assess, route, and recover. In that sense, resilience is not separate from trading efficiency. It depends on it.